Flood Insurance

Flood Insurance

FLOOD INSURANCE__DO I NEED IT? The world is seeing all kinds of crazy weather these days. I remember the "Mother's Day" flood in 2006 when it rained 13 inches in two days. I couldn't get out of y road for a week. So you never know.

FEMA has recently updated their maps to determine what properties are considered in a Flood Zone. This impacts you as a buyer since a lender will not provide a mortgage without a flood insurance rider paid for in advance of the closing if one is needed. And it isn't cheap. It doesn't mattter if you are married to the insurance broker--the cost is dictated by the federal government. You may be able to get a high deductible. We are still talking about a policy that could cost between $1,000 - 1,700 a year.

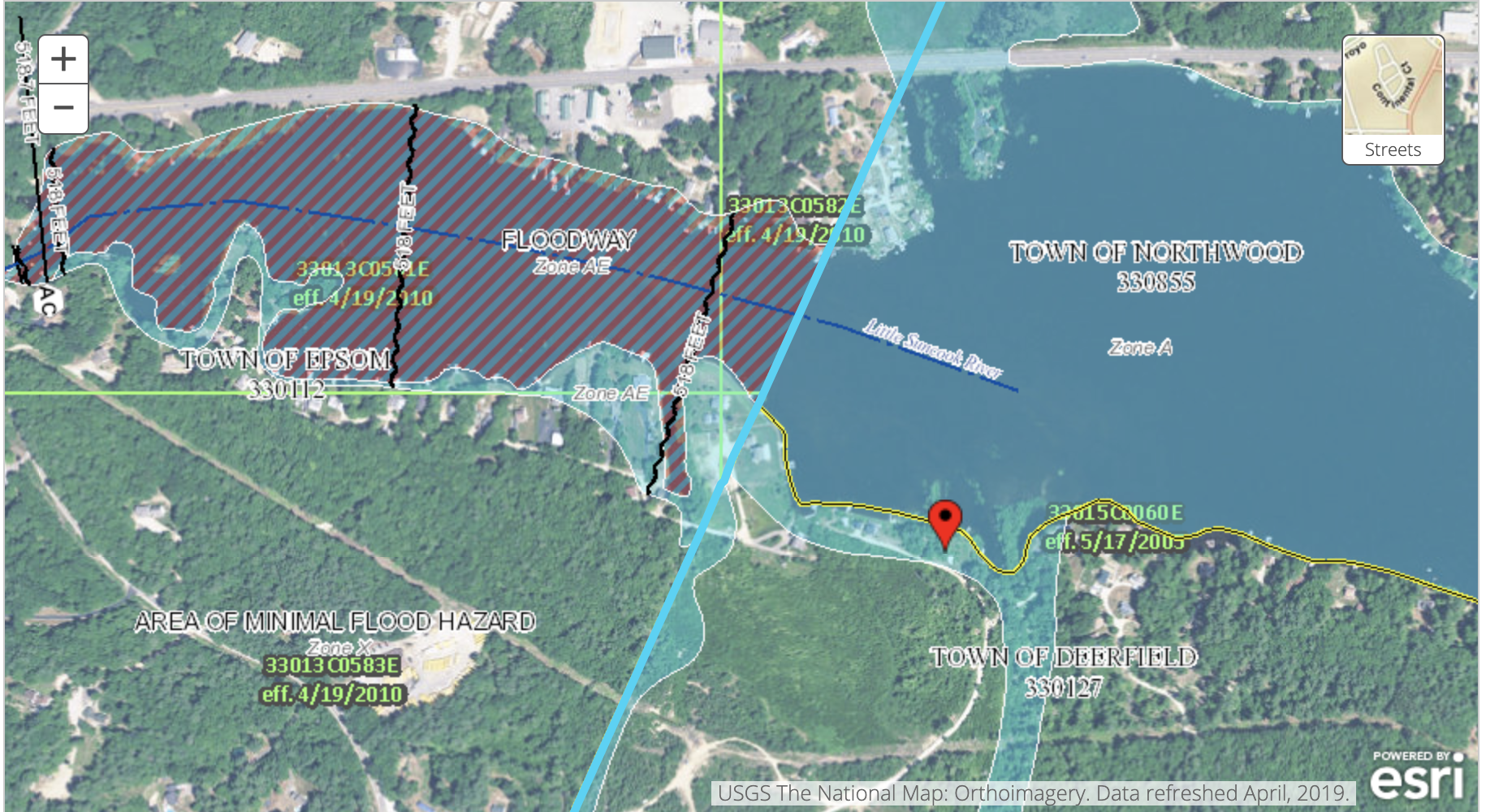

WHAT IS A FLOOD ZONE PROPERTY? Some guy in a dark government room looks at available data and arial photos and draws a rough line around a lake. Go to the FEMA site and plug in an address of the property you are considering to buy at: www.FEMA.gov. I have had listings that wouldn't flood even if NOAH was building an Arc, and there was a reverse gravitational pull on the earth. See your own home on a FEMA map https://experience.arcgis.com/experience/e492db86d9b348399f4bd20330b4b274/page/Page/?views=Sea-Level-Dataset%2CCurrent-Conditions

SO WHAT HAPPENS IF THE PROPERTY IS CONSIDERED IN A FLOOD ZONE? First you would need an "elevation certificate" which can be performed by a qualified surveyor. If the house on the lake shows to be higher than the spillover height (in the case of a lake held back by a dam) or by other factors that can determine the maximum lake height, then the surveyor can send to FEMA a form to adjust the flood zone maps--(which takes about 6-8 weeks) If FEMA accepts the findings, then your property will not require flood insurance again. Don't expect a seller to even know about this problem, or to have acquired a elevation certificate. Most sellers would put in their disclosures that their house is not in a flood zone if they are not currently paying for flood insurance. Certainly a current owner wouldn't voluntarily let their insurance company know that their house in a flood zone so they could have the privilege of forking out $1700 a year for insurance. What you need to know as a buyer is to find out before you make an offer on a property if flood insurance is going to become an issue.

Here is some info about Flood Insurance

Here are some Flood Insurance Basics.

Connect